We use cookies to provide you with the best possible online experience. Read our cookie policy.

Media Release

04 March 2026

Business confidence on the mend

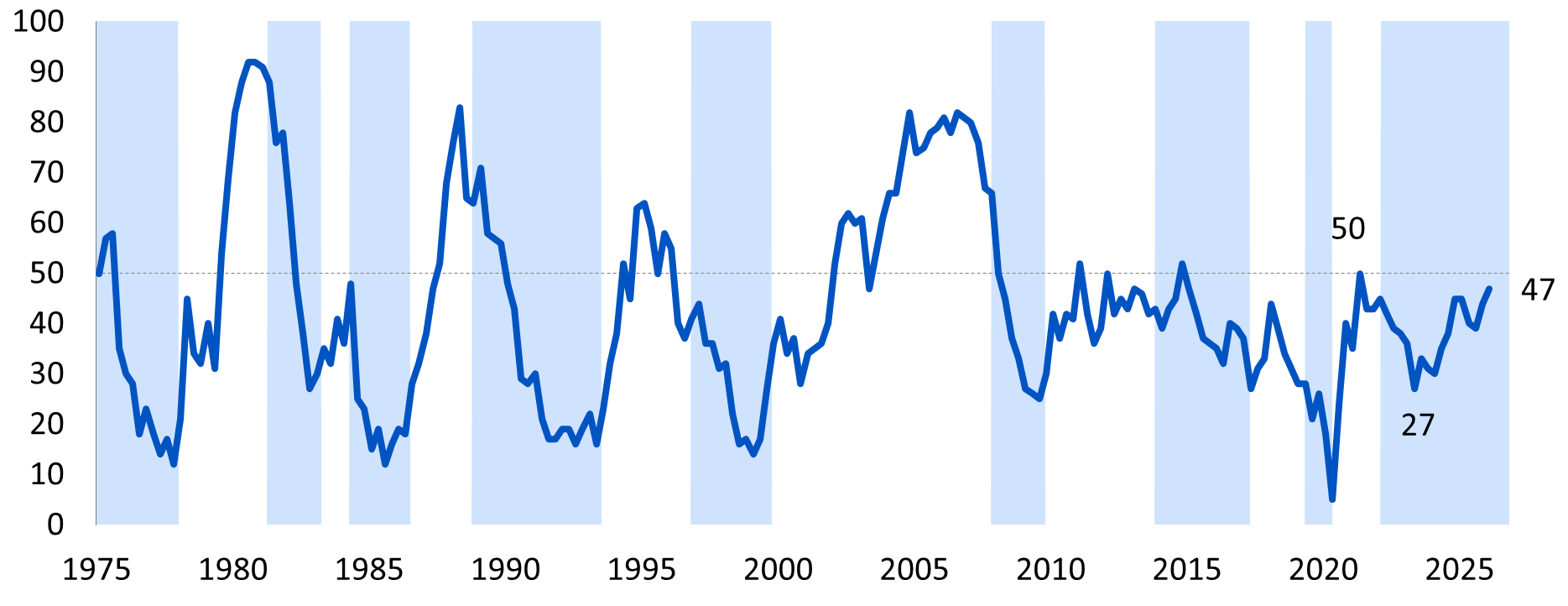

The RMB/BER Business Confidence Index (BCI) rose by a further 3 points to 47 in the first quarter of 2026, building on the improvement in the fourth quarter of 2025. The BCI now stands six points above its long-term average and a solid 20 points above the post-COVID low reached in 2023Q2. Barring the post-COVID recovery, this is the highest confidence reading since 2015.

Figure 1: RMB/BER Business Confidence Index (BCI)

% satisfactory

Source: BER, SARB (shaded areas represent economic downswings)

The survey took place from 12 to 23 February 2026. Sentiment was supported by a generally well-received State of the Nation Address (SONA), delivered at the start of the survey period, as well as the continued stability of the Government of National Unity (GNU) ahead of the Budget, delivered on the 25th of February. Any shifts following the Budget therefore fell outside the survey window, but would, on balance, likely have supported sentiment.

The rand is 7% stronger against the US dollar relative to the fourth quarter of last year, which is positive from a cost perspective, though weighs somewhat on export competitiveness. Although the South African Reserve Bank (SARB) left the policy rate unchanged in January, the repo rate remains 100 basis points (bps) below its level a year ago, and while the 10-year government bond yield has declined by 70bps since the fourth quarter BCI, it is roughly 200bps lower relative to a year ago. This maintains a meaningfully more supportive interest-rate environment compared to both the last quarter and to a year ago.

That said, the backdrop was not without challenges. Geopolitical tensions intensified amid concerns about a potential escalation of conflict between Iran and both Israel and the United States. Domestically, the water crisis in Gauteng worsened; Limpopo and Mpumalanga were affected by flooding; and the foot-and-mouth disease (FMD) outbreak persisted. In addition, available high-frequency official data points to a loss of momentum in the production side of the economy during 2025Q4. This is somewhat unexpected given the more positive underlying activity data from survey results during this period. The extent of this possible slowdown will be clarified by Statistics South Africa’s GDP release next week.

Details

The improvement in the composite index was not broad-based despite market sentiment being generally positive. Confidence among manufacturers and retailers declined after encouraging gains in the last quarter. However, solid increases among new vehicle dealers, wholesalers and building contractors more than offset these declines, leaving the overall index higher, both quarter-on-quarter and compared to a year ago (2025Q1).

Table 1: Business confidence per sector

|

Indicator |

LT avg. |

24Q1 |

24Q2 |

24Q3 |

24Q4 |

25Q1 |

25Q2 |

25Q3 |

25Q4 |

26Q1 |

change |

|

RMB/BER Business Confidence |

41 |

30 |

35 |

38 |

45 |

45 |

40 |

39 |

44 |

47 |

3 |

|

New vehicle dealers |

39 |

16 |

10 |

27 |

23 |

52 |

42 |

54 |

58 |

67 |

9 |

|

Wholesalers |

45 |

37 |

53 |

51 |

60 |

42 |

50 |

38 |

42 |

50 |

8 |

|

Building contractors |

40 |

42 |

47 |

41 |

51 |

45 |

35 |

46 |

39 |

50 |

11 |

|

Retailers |

40 |

34 |

39 |

45 |

54 |

50 |

42 |

32 |

43 |

36 |

-7 |

|

Manufacturers |

34 |

21 |

28 |

28 |

36 |

34 |

33 |

23 |

39 |

30 |

-9 |

Source: BER

New vehicle dealers remained the most optimistic sector, with a notable further increase in sales underpinning a 9-point rise in sentiment to 67. Confidence in the sector has now surpassed the post-COVID peak of 63 points, recorded in 2021Q2, to reach a 13-year high.

Wholesalers, which are also partially consumer-facing, saw confidence rise by 8 points to 50, marking its best level since late 2024. The increase was supported by solid improvements in business conditions and higher sales volumes.

However, not all consumer-facing sectors performed well. Retailers took a breather at the start of the new year, with retail confidence declining by 7 points to 36, as base effects began to weigh on annual growth rates. This is slightly below retail confidence’s long-term average of 40. Sales volumes softened for non-durables and durables, while semi-durables performed somewhat better in the first quarter.

Positively, building contractors recorded a significant 11-point increase in confidence to 50. The improvement was supported by an improvement in activity, although the non-residential sector continues to outperform the residential sector.

Manufacturers were the laggards, with confidence in this sector declining by 9 points to 30. This partially reverses the welcome uptick in the fourth quarter of last year. The sector continues to grapple with weak demand conditions, which are insufficient to generate a sustained recovery in output. Encouragingly, forward-looking investment indicators remain relatively upbeat.

Bottom line

According to Isaah Mhlanga, Chief Economist at RMB, “the further increase in the composite RMB/BER BCI is encouraging. Sustained improvements in confidence are needed to kick-start fixed investment, and the current above-average level suggests we may well see a rebound in capital expenditure during 2026. However, there is a risk that the recovery is becoming less balanced.”

“Manufacturers are particularly sensitive to overall demand dynamics, and their subdued confidence suggests that improved sentiment elsewhere has not yet translated into stronger domestic demand,” says Mhlanga, while acknowledging that forward-looking indicators point to some improvement.

The political stability of the GNU remains crucial to sustaining structural economic reforms and improved business sentiment. However, many respondents continue to flag operational challenges at local ports, while concerns about cheap imports are increasingly being raised. Geopolitical developments, largely beyond South Africa’s control, also remain top of mind for many businesses.

A sustained improvement in confidence will ultimately depend on stronger demand, continued policy credibility and progress on structural reforms. For now, sentiment is improving but translating that into durable growth remains the key test for 2026.

Fourth-quarter 2025 GDP figures, to be released by Statistics South Africa next week, will confirm whether the improvement in BCI over the last two quarters is translating into faster growth, despite evidence from high-frequency indicators that suggests growth may have struggled over this period.

Ends

Enquiries:

Isaah Mhlanga

Chief Economist

Tel: 073 736 5357 / 011 282 1460

Isaah.Mhlanga@rmb.co.za